Weekly Market Commentary

THE WEEK IN REVIEW: November 10, 2024 – November 16, 2024

Markets moved up quickly, but they’ve stalled for now

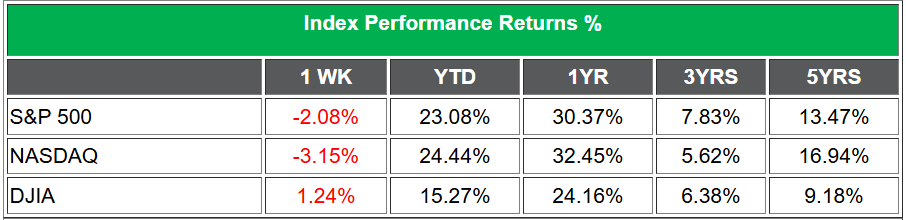

The market took a bit of a breather last week after spiking upward immediately after the election. The Dow pierced 44,000 points, the S&P 500 hit 6,000, and the Nasdaq rose above 19,000 for the first time ever. 1,2,3 After concerns about a possibly prolonged and drawn-out ending to the election were dispelled and uncertainty over the results dissipated, Republicans ran the table and took full control of the presidency and both branches of Congress.4 Plus, the new Trump administration has begun putting forward its nominees for key cabinet posts.5 Whether all these folks get confirmed remains to be seen, but the mandate for change was unambiguous and there will likely be a lot of new policy stances going forward.

First up will be a possible extension of the Trump tax cuts (perhaps permanently). We may also see President-elect Donald Trump follow through on his promises regarding taxes on tips, Social Security and overtime. Some analysts feel these things will increase our deficit and national debt, and maybe they will. However, Trump has already set forth tasks for the Department of Government Efficiency (DOGE) to look for ways to streamline government and cut unnecessary costs.6

We may also see the energy industry ramp up as Trump follows through on his “Drill, baby, drill” pledge to restore our energy independence (and, as some are saying, energy “dominance”).7 Higher energy prices have been a direct contributor to inflation, and hopefully lower energy prices will finish what the Federal Reserve has been trying to do and get us to an inflation rate of 2% or below. Then there’s deregulation, a staple of the first Trump presidency. As we cut unnecessary government spending, the goal is to also cut burdensome regulations, spurring economic growth and leading to prosperity.

Finally, there are the tariffs. Much has been made that additional tariffs will cause inflation. Again, that may be the case.8 But the last time Trump was president, he used tariffs as a negotiating tool to get other countries to behave differently and inflation did not go up. True, imposing blanket tariffs on everything from everywhere would likely be inflationary, but he didn’t do that in the past. This is one area that will bear watching.

There are other areas that may impact the economy and markets, but there aren’t many direct points of reference yet. Specifically, what impact will Trump’s immigration policies have on the costs of labor, housing and food? We need to keep a close eye on this area, as well.

As mentioned earlier, markets took a breather last week, but it seems the momentum is there for a continued run through the end of 2024. Some of the moves defy logic, like Tesla ripping. Trump hasn’t been a supporter of electric vehicles (EVs), but maybe Elon Musk’s proposed role in the administration is the reason. However, it’s still illogical given that Trump wants to remove the current subsidies for EVs.9

Another typical sign of irrational melt-up is Bitcoin, which has jumped over 30% since the election.10 Trump is supportive of Bitcoin and cryptocurrencies in general, but that shouldn’t make it worth 30% more overnight. This isn’t a time to be over-extended, and if your portfolio is out of whack, we recommend rebalancing to target. If you have realized losses, you may want to consider using them to offset capital gains. If you don’t have losses and only gains, it might be good to ride out the year and rebalance first thing in 2025 so you have the rest of the year to help manage your tax situation.

Rates and inflation remain stubbornly higher

If anything is going to spoil the market rally, it will probably be interest rates. The 10-year Treasury has been closing in on 4.5%, even though the Fed just cut short-term rates.11 This should serve as a cautionary development. Once you start seeing 4.5% or 5% yield on a government bond 10 years out, people begin to take notice and usually stocks suffer due to the resulting volatility.

Despite the cuts in short-term rates, the bond market is telling us they aren’t expecting deficits or the debt to decline anytime soon and they are demanding higher yields as a result. Also, inflation isn’t where we need it to be, yet the Fed cut rates just a week before we saw the Consumer Price Index (CPI) creep up from 2.4% to 2.6%.12 The Producer Price Index (PPI) also jumped from 1.9% to 2.4%.13 Although the readings were mostly expected, it still shows we aren’t close enough to where we need to be with inflation.

Fed Chair Jerome Powell spoke last Thursday and told folks the Fed doesn’t need to “be in a hurry” to cut rates — yet the markets still expect another 25-basis-point (0.25%) cut in December.14,15 Powell seems to be flummoxed; after cutting rates twice since September, the bond markets have mostly ignored the Fed while the stock market assumed there would be more cuts and priced them in. Someone is going to be wrong, and it could be the stock market, given the run-up we’ve seen in recent weeks.

It will take some time for this all to play out. It seems like we’re good through year-end, but we need to monitor data. If we start seeing a deterioration in the economy, the stock market could stumble and the bond markets would be proven correct.

Coming This Week

- After an avalanche of events and data, it will be refreshing to get a breather this week and most of next week with the Thanksgiving holiday coming up. The election is over, and the Fed cut rates again, with expectations for another quarter-point cut next month. However, that might not happen, given where inflation is currently. The most current reading of the CPI at 2.6% has confirmed the decline in the rate of inflation has all but stalled around those levels, and it will take something more to push us to 2%. Hopefully, it won’t involve a Fed reversal now that they’ve started cutting, but it’s unclear how additional rate cuts would push inflation closer to 2%.

- We won’t see any significant data until midweek, when we’ll get the MBA Mortgage applications, which will look at the condition of the real estate market.

- On Thursday, we’ll see the latest weekly unemployment claims, the Philly Fed manufacturing index and existing home sales.

- Finally, we will get consumer sentiment on Friday to end a light week of data.

- With all the recent excitement, third-quarter earnings have flown under the radar.16 So far, 91% of the S&P 500 has reported actual results, with 75% reporting positive earnings per share (EPS) and 60% reporting positive revenues. Earnings growth for the third quarter for the S&P 500 is 5.3%, the fifth straight year-over-year earnings growth for the index. Overall, it’s been a stellar earnings season; Wall Street was expecting 3% earnings growth, but we are seeing nearly double that. The phenomenon has created a very strong base for the markets to continue their rally.

Sources:

1 Yahoo! Finance. “Dow Jones Industrial Average (ˆDJI).” https://finance.yahoo.com/quote/%5EDJI/. Accessed Nov. 17, 2024.

2 Yahoo! Finance. “S&P 500 (ˆGSPC).” https://finance.yahoo.com/quote/%5EGSPC/. Accessed Nov. 17, 2024.

3 Yahoo! Finance. “NASDAQ Composite (ˆIXIC).” https://finance.yahoo.com/quote/%5EIXIC/. Accessed Nov. 17, 2024.

4 Scott Wong. NBC News. Nov. 13, 2024. “Republicans win the House, NBC News projects, as Trump’s party takes full control of Washington.” https://www.nbcnews.com/politics/2024-election/republicans-win-house-majority-trump-party-senate-control-rcna179231. Accessed Nov. 17, 2024.

5 Kathryn Watson and Caitlin Yilek. CBS News. Nov. 16, 2024. “See the list of Trump Cabinet picks and more White House appointments so far.” https://www.cbsnews.com/news/who-might-be-in-donald-trump-cabinet/. Accessed Nov. 17, 2024.

6 Aimee Picchi. CBS News. Nov. 14, 2024. “What to know about Trump’s Department of Government Efficiency, led by Elon Musk and Vivek Ramaswamy.” https://www.cbsnews.com/news/trump-department-of-government-efficiency-doge-elon-musk-ramaswamy/. Accessed Nov. 17, 2024.

7 Michael Copley. NPR. Nov. 6, 2024. “Trump’s victory promises to shake up U.S. energy and climate policy, analysts and activists say.” https://www.npr.org/2024/11/06/nx-s1-5181891/trump-win-climate-change-fossil-fuels-clean-energy. Accessed Nov. 17, 2024.

8 Dr. Jeffrey Roach. LPL Financial. Nov. 13, 2024. “Are Tariffs Always Inflationary?” https://www.lpl.com/research/blog/are-tariffs-always-inflationary.html. Accessed Nov. 17, 2024.

9 Chris Isidore. CNN Business. Nov. 15, 2024. “Trump may end the $7,500 EV tax credit. Elon Musk and Tesla would reap the rewards.” https://www.cnn.com/2024/11/15/business/musk-tesla-trump-ev-tax-credit/index.html. Accessed Nov. 17, 2024.

10 Yahoo! Finance. “Bitcoin USD (BTC-USD).” https://finance.yahoo.com/quote/BTC-USD/. Accessed Nov. 17, 2024.

11 CNBC. “U.S. 10 Year Treasury.” https://www.cnbc.com/quotes/US.10. Accessed Nov. 17, 2024.

12 U.S. Bureau of Labor Statistics. Nov. 13, 2024. “Consumer Price Index Summary.” https://www.bls.gov/news.release/cpi.nr0.htm. Accessed Nov. 17, 2024.

13 U.S. Bureau of Labor Statistics. Nov. 14, 2024. “Producer Price Index News Release summary.” https://www.bls.gov/news.release/ppi.nr0.htm. Accessed Nov. 17, 2024.

14 Ann Saphir and Howard Schneider. Reuters. Nov. 14, 2024. “Powell says no need for Fed to rush rate cuts given strong economy.” https://www.reuters.com/markets/us/powell-says-no-need-fed-rush-rate-cuts-given-strong-economy-2024-11-14/. Accessed Nov. 17, 2024.

15 CME Group. “FedWatch.” https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html. Accessed Nov. 17, 2024.

16 John Butters. FactSet. Nov. 8, 2024. “Earnings Insight.” https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_110824.pdf. Accessed Nov. 17, 2024.

Securities and advisory services offered only by duly registered individuals of Madison Avenue Securities, LLC (MAS), member FINRA/SIPC and a registered investment advisor. MAS and Vineyard Financial are not affiliated entities.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

11/24 – 3991358-3

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.