Weekly Market Commentary

THE WEEK IN REVIEW: August 18, 2024 – August 24, 2024

Fed takes its foot off the gas

The Federal Reserve’s annual symposium continues to be a significant news-making event in between their regular meetings. Central bankers from around the world flew into Jackson Hole, Wyoming, last week to attend what has become the globe’s premier economic gathering.

Officially, the event is called the “Kansas City Federal Reserve’s Annual Symposium” and is held in Grand Teton National Park. The Kansas City Fed started it in 1978 with an initial focus on agriculture, but after a few years, the organizers decided to broaden the meeting’s scope to attract bigger names. The meeting was originally held in Kansas City but moved to Jackson Hole in 1982 to entice then-Fed Chair Paul Volcker (a flyfishing devotee) to join.

In 2022, current Fed Chair Jerome Powell kneecapped a struggling stock market with a short speech at the symposium, where he said not to expect the Fed to stop raising rates because they weren’t done. Rates subsequently doubled from those levels and killed a recovery rally in stocks that year.

Comments following this year’s symposium were more encouraging. In what will probably go down in history as the “Time Has Come” speech, Powell said we should expect rate cuts to begin at their next meeting in mid-September. Minutes from the July meeting showed a couple of Fed governors were ready to cut rates in July, and the “vast majority” thought a September rate cut was warranted based on the data’s trajectory.

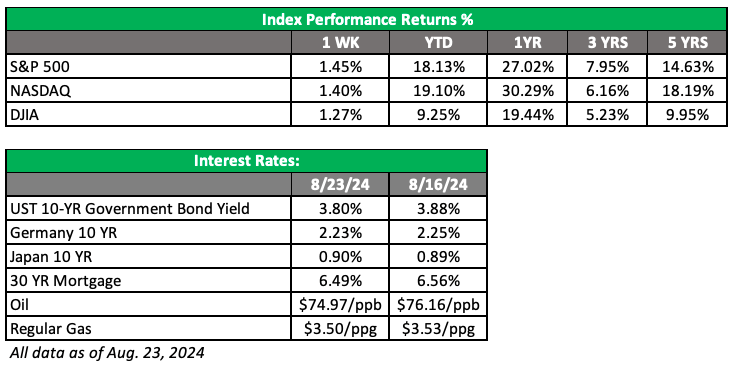

From a data perspective, the economy was hanging in there through the first half of the year and job growth was still robust. Markets adjusted to the lower expectations for rate cuts, realizing there really was no justification even as the economy felt weak and jobs started to wane. But that all changed last month; the market sent a clear message about recession worries and the data was decidedly weaker, especially jobs. With the Consumer Price Index (CPI) dipping below 3%, it seems the Fed has decided “the time has come” for cuts.

Rate cuts are here — so now what?

In January, we expected six or seven rate cuts in 2024, but the Fed told us to expect two or three. It’s likely that once the cuts start in September, we’ll see additional cuts at the final two Fed meetings in November and December and that the cuts will continue into 2025.

A couple of weeks ago, there was a lot of handwringing and worry, with people screaming for an emergency 50-basis-point (0.50%) rate cut between Fed meetings. Now markets are within a whisker of their all-time highs, and Powell has said to expect cuts at the next meeting.

We are primed for takeoff in the final four months of the year. How might that play out? First, as soon as Powell said the “time has come” last Friday, stocks rallied and yields dipped. The initial high for the markets will give way to debates about the significance and magnitude of the cuts. Is a quarter-percent cut a piddly amount? Is a half-percent cut appropriate at this time or is something worse afoot that the Fed knows about and is trying to correct? As we’ve said before, the market is fickle and always on to the next thing.

Given the Fed’s history of moving too late and its checkered record with “soft landings,” much has been made of the fact that markets declined after rate hikes. In those cases, we had already entered a recession, and it seemed as if the Fed was simply too late. That likely won’t be the scenario here, but four months is a long time, and we still have global turmoil and an election here at home. Volatility could remain elevated, and we may see more ups and downs than we did in the first half of the year.

However, “the time has come,” and we are likely going to see a less restrictive monetary environment, which usually bodes well for stocks. The soft landing is in play. Let’s just hope the Fed has remembered to lower the landing gear.

Coming this week

- The last week in August should be downright dull compared to the rest of the month. We’ll get the latest numbers on durable goods (Monday), the Case-Shiller home price index and consumer confidence (Tuesday) and MBA mortgage applications (Wednesday).

- On Thursday, we’ll see the latest unemployment claims and pending home sales. We’ll also get the second reading of second-quarter gross domestic product (GDP), which initially came in at 2.8%.

- Finally, we’ll get personal income and personal consumption expenditures (PCE) on Friday. The Fed really likes this measure of inflation, so it should give us even more insight into the Fed’s next move.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

8/24 – 3757920-4

Ready to Take The Next Step?

For more information about any of our products and services, schedule a meeting today or register to attend a seminar.